Capitalism needs a healthy dose of socialism to survive.

The winds of change are gaining strength. Alexandria Ocasio-Cortez (AOC), a rookie congresswoman from New York, has unveiled a vision for a Green New Deal while proposing a 70 percent tax on income over $10 million. Even establishment voices are joining the chorus, with newspapers such as Forbes and Business Insider publishing pieces highlighting the heights of wealth inequality in America. And when the New York Times puts an op-ed entitled Abolish Billionaires above the fold, as it did in February 2019, you know something is truly afoot.

That article followed on the heels of the World Economic Forum’s annual summit at Davos, a Swiss alpine resort where the masters of the universe convoke each January to rub shoulders and confabulate on the state of the world. The difference this time was that a few progressive iconoclasts were also in attendance. They made themselves heard.

Rutger Bregman, an historian, provided the most viral soundbite. He remarked that conversations around inequality should focus on taxes rather than philanthropy, and that “all the rest is bullshit.” The consequent gasp that swept through the room, as well as the BBC’s apology for subjecting its viewers to his blasphemy, speaks volumes. How delicate one must be to find offence in such a trivial word. Then again, when you’ve paid at least $200k to attend a Davos industry session, you would rather not be accosted by peasants’ crude barbarisms. (One wonders how much longer they will be permitted entry, should their philistine behaviour continue. Better to save the world in private, like the Bilderberg Club.) No, you would much prefer to marinate in the musings of real “thought-leaders.”

Like Michael Dell, whose $30 billion+ fortune puts him among the richest human beings on our planet. Sitting on a Davos discussion panel, he was confronted by the unpleasant question of whether he supported AOC’s tax proposal. Dell replied that his private charitable foundation has donated more to causes than what the new tax on his income would raise, and added that, in any case, his foundation can “allocate those funds” better than the government can.

Rather convenient answers from a man who, like most plutocrats, is keen to remain perched safely on the moral high ground as the tide rises around him. The world’s very wealthiest citizens make the bulk of their fortunes from capital gains and investment dividends, not labour income that would be taxed under AOC’s plan. And while he might have a case in some respects when he says he can spend his money more intelligently than the government can, this, too, is beside the point. St. Augustine’s proverb that “charity is no substitute for justice withheld” holds fast. Private philanthropy, however admirable, does not obviate progressive taxation.

American democracy operates according to the Golden Rule: Those with the gold make the rules.

There are some tasks for which the government is simply better suited than private citizens, such as funding large infrastructure projects (which are desperately needed across the U.S.), universal healthcare, or even, someday, a national basic income. Even someone of Dell’s stratospheric means cannot make any of those things happen single-handedly. Moreover, were he truly as magnanimous as he wishes to appear, he would have committed to give away at least half his wealth as part of Bill Gates’ and Warren Buffet’s Giving Pledge. Even though charity does indeed do good in the world, it cannot be the primary solution. On the contrary, “the proper aim,” as Oscar Wilde put it, “is to try and reconstruct society on such a basis that poverty will be impossible.”

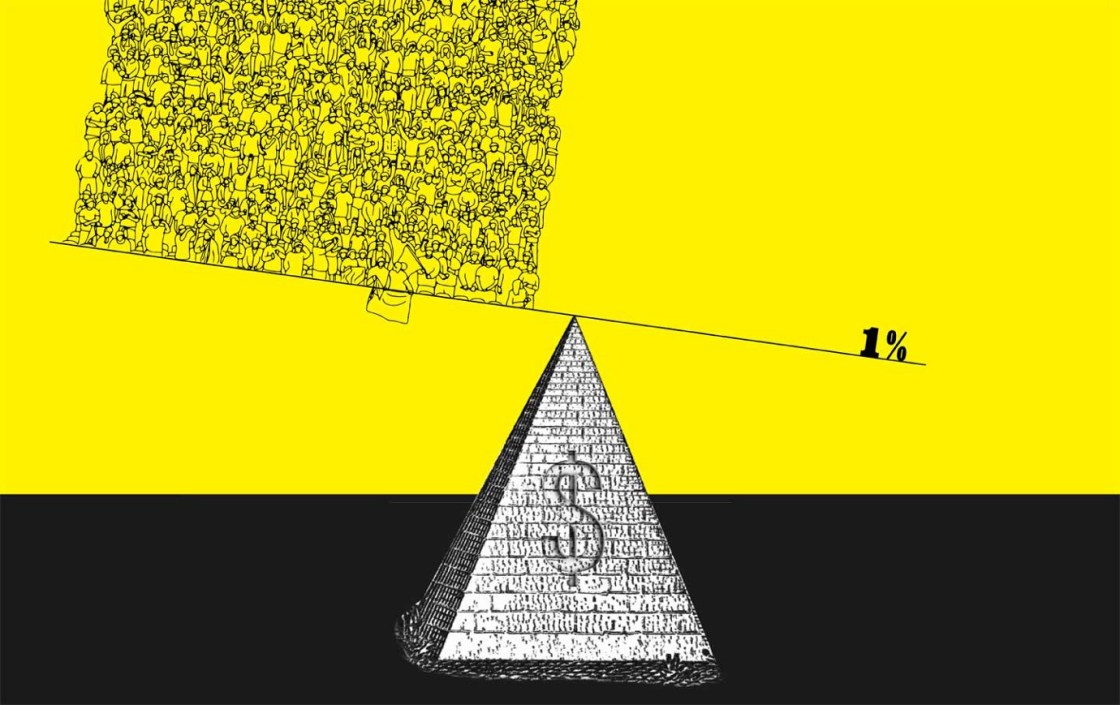

Poverty in our age is both democratic and economic. A society in which a few wealthy citizens exert disproportionate influence over public policy for the masses can’t reasonably be called a true democracy. At the same time, enormous wealth inequality is hampering economic growth. Capitalism’s excesses must be tempered with socialistic elements if it is to be sustained long-term. Steeply progressive taxation equips the communal purse to begin the needed reconstruction.

Two Worlds

If we define democracy as majority rule, America doesn’t truly qualify. The average person has next to no influence on public policy. According to a 2014 study by Martin Gilens and Benjamin Page on the impact that elites, interest groups, and ordinary citizens have on the American political process:

When a majority of citizens disagrees with economic elites or with organized interests, they generally lose. Moreover, because of the strong status quo bias built into the U.S. political system, even when fairly large majorities of Americans favor policy change, they generally do not get it.

In politics, money is nearly everything. Yes, Jeb Bush learned the hard way that not even a $130 million war chest can get you elected when you’ve got less charisma than socks in sandals. But he needed money just to get on the stage. It takes billions of dollars to become president, and even in U.S. congressional races, the candidate who spends the most money usually wins. Much of those funds come from special-interest groups with specific agendas, and politicians are reluctant to bite the hands that feed them. The fact that senators and congresspeople are expected to spend an absurdly large part of each workday fundraising for the next election shows that American democracy operates according to the Golden Rule: Those with the gold make the rules.

There are, in effect, two worlds. Most of us live in one; the super-rich inhabit the other. They use private means of transportation; they participate in exclusive, invitation-only social events (like Davos); they’re able to purchase special access to elite institutions — see the recent college admissions bribery scandal; and they’re less likely to face severe repercussions for their misdeeds.

Take Paul Manafort, the unsavoury political consultant whose least corrupt client was probably Donald Trump. Despite facing a recommended jail sentence of 19 to 24 years for perjury, money laundering, and fraud in his first trial, Manafort was given less than 4 years in prison. The presiding judge was legally obliged to hand down a sentence comparable to similar cases, but former federal prosecutor Ken White explains that “even when rich people get convicted, money helps get them the best plea deals, the most persuasive sentencing presentations, and often the most lenient sentences.” Meanwhile, thousands of inmates in the U.S. are serving life-without-parole sentences for non-violent drug and shop-lifting crimes — the crimes of the poor.

Then there’s the case of soccer superstar Cristiano Ronaldo, who is alleged to have raped a woman in a Las Vegas hotel room in 2009. In an attempt to buy her silence, he settled with her out of court for $375,000 — equivalent to one week of his salary at the time. According to German newspaper Der Spiegel, it appears that the payment was wired from the bank account of a company “based in the tax haven of the British Virgin Islands, a company that had kept Ronaldo’s advertising and sponsoring revenues for years.” Most people don’t have offshore accounts nestled in tax havens, which are estimated to hold 10 percent of world Gross Domestic Product (GDP), or about $8 trillion. For most people, including Ronaldo’s accuser, $375,000 is a life-changing sum of money. For a select few, though, it’s pocket change. Massive wealth buys tremendous privilege.

A Simple Equation

The plutocratic elite may not be concerned with preserving true democracy, but even they depend on having a functioning economy from which to profit. That will soon become impossible unless action is taken to redistribute a significant amount of wealth. The developed world appears to be suffering from a malaise known as secular stagnation, or sluggish long-term economic growth. In a nutshell, too much money is being saved, and not enough is being invested in productive activities to drive sustainable economic expansion.

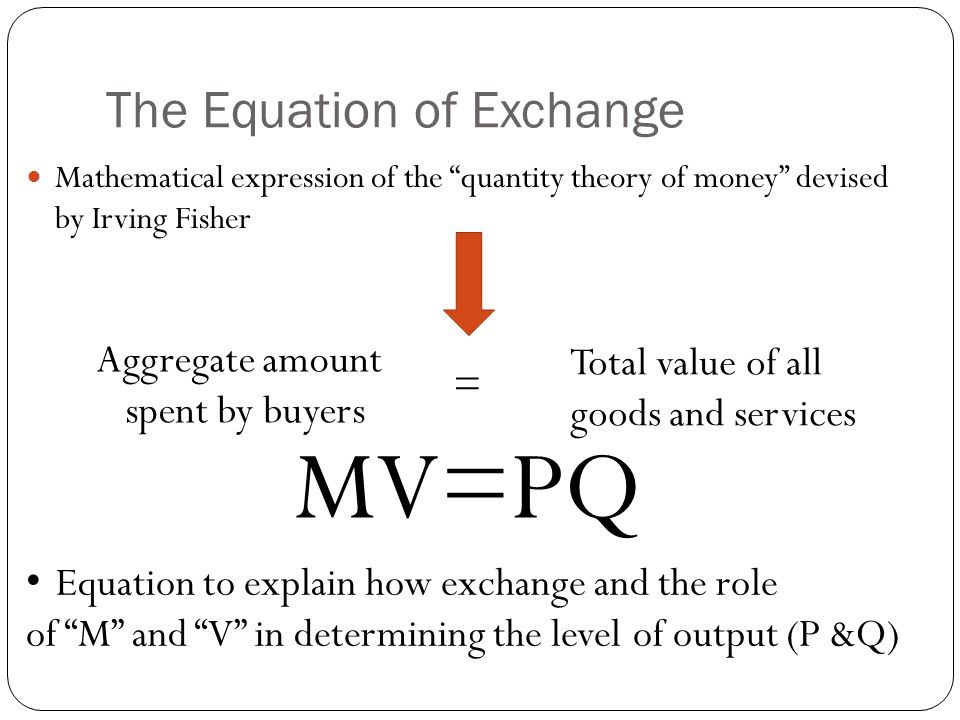

Fundamentals show why. The formula MV=PQ is called the equation of exchange. The economy’s supply of money (M) multiplied by the velocity at which that money changes hands (V) accounts for all the money spent on purchases. The price level (P) multiplied by the quantity of all goods and services transacted (Q) accounts for the total value of all sales. Since, by definition, purchases must equal sales, the equation is always in balance. Q is the same as GDP.

People in most mature western economies are living longer than they used to. Meanwhile, birth-rates in these places are declining as people marry later in life and families have fewer children on average. The labour force as a share of the population will not grow over the next twenty years, meaning less investment in capital to equip that shrinking pool of workers. At the same time, where Blockbuster once hired people to build its brick-and-mortar stores and stock its shelves, Netflix now provides the same services with far less tangible overhead; the new digital economy has reduced overall investment. Even if these trends are contributing to an economic dilemma, though, there’s no reason to turn back the clock.

The opposite side of the ledger is a different story. The equation of exchange shows enormous wealth inequality is partly responsible for the savings glut that is retarding growth. Unlike the tyrannical social engineering or neo-Luddism that would be required to remedy the investment issues, reducing disparity in society is both desirable and feasible.

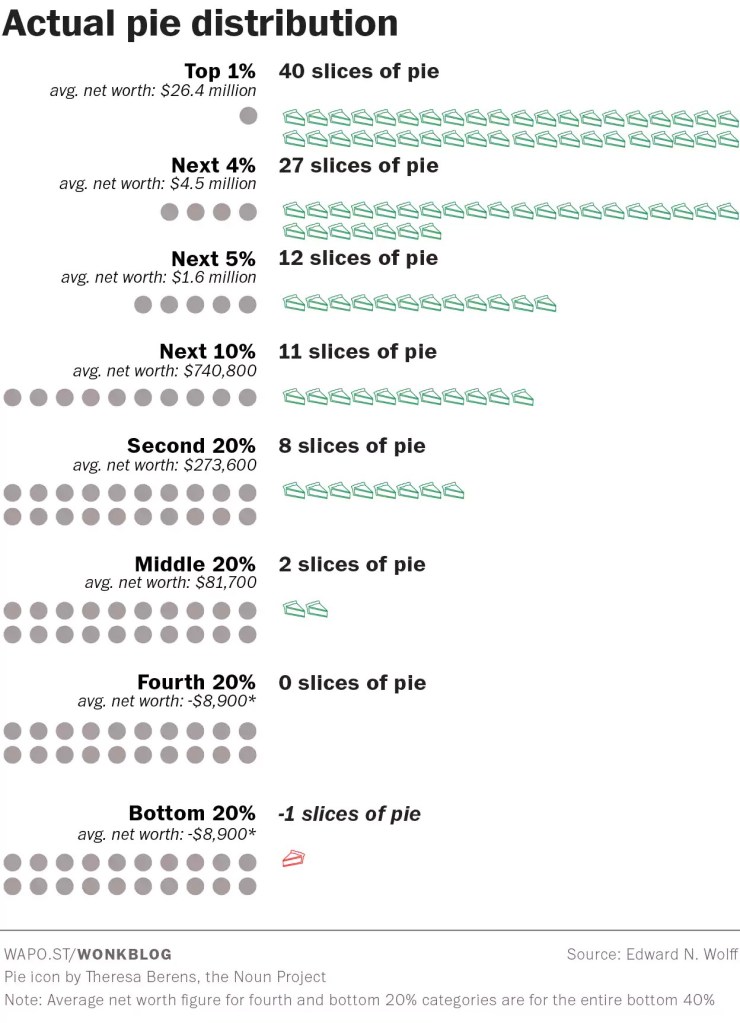

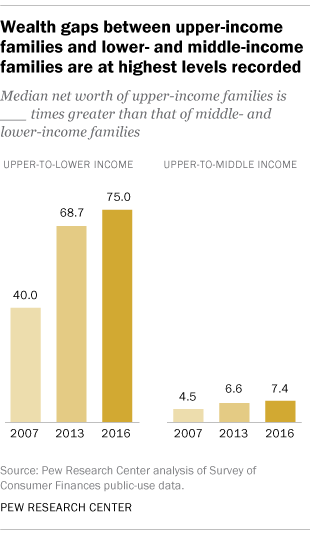

Nearly half of all Americans and Canadians live paycheque to paycheque. These “working poor” are forced to spend all their disposable income and save none, so the velocity of their money is high. Very rich people, by contrast, have more money than they know what to do with. After meeting their basic needs, and spending some money on luxuries, they save a significant portion of their wealth in assets (so the overall velocity of their money is low). Since the richest hundredth of Americans owns 40 percent of the country’s wealth, and the richest tenth owns nearly 80 percent (Figure 1), a huge share of capital is saved instead of spent.

Another implication of wealth inequality is debt. When a person without savings encounters a financial emergency, they are forced to borrow money. The interest they pay on that loan is money they would have otherwise spent in the future. From the economy’s point of view, in other words, paying down debt is equivalent to saving. You’ll notice in our equation that if M and P remain constant, then a drop in V will slow economic activity, Q.

Overall, excessive savings combined with insufficient investment drives down the interest rate at which the supply of money to borrow, and the demand for it, are in equilibrium. In the United States this trend has been in force for decades (Figure 3).

An excessively low interest rate is damaging in a number of ways. When the rate of return on savings bonds is low, investors pile their money into assets offering higher returns, like real estate, increasing the risk of a market bubble. Secular stagnation is also contagious, because when capital flees to seek out higher returns elsewhere, it drives down interest rates in those new places as well. Worst of all, a rock-bottom interest rate diminishes policy-makers’ ability to respond to crisis.

Running Out of Solutions

The ostensibly reliable value of the U.S. housing market has long been used as collateral to underwrite a great deal of derivative financial securities. That assumption collapsed when the market tanked in 2007, snatching the rug out from under many of the world’s largest investment banks whose portfolios were exposed to toxic assets. Suddenly, no one was able to pay their creditors, so banks stopped lending in such a risky environment. The contagion of debt defaults ricocheted down Wall Street. The United States, and much of the world to which it is connected, plunged into a deep recession. It was central banks’ time to shine.

In this era of secular stagnation, rapid economic growth is an illusion.

When a central bank wants to stimulate the economy, the conventional method is to cut the key interest rate in order to make money cheaper to borrow. The problem is that interest rates cannot be reduced if they are already near zero. That is the situation in which several of the largest central banks around the world, including the U.S. Federal Reserve (the Fed), all found themselves in the wake of the 2008 financial crisis. Deprived of the traditional methods for stimulating their economies, they were forced instead to turn to an unconventional tactic known as Quantitative Easing (QE), a fancy name for creating new money out of thin air and using it to purchase financial assets that no one else wanted. In doing so, the stimulus aimed to revive the price of those assets and replenish liquidity in the banking sector to get people trading and lending again. In 2007, the size of the Fed’s balance sheet was $870 billion. By the time it had reached the apogee of its QE program in 2015, the asset side of its balance sheet had ballooned to $4.5 trillion. The Fed had increased the U.S. money supply dramatically.

Returning once more to the equation of exchange, notice that if M increases while V and Q remain constant, P must rise commensurately; that’s inflation. Noting this fact alongside the Fed’s giant balance sheet expansion, the prominent economist Larry Summers remarks that:

Had economists been told [before the crash] that such monetary policies lay ahead…they would have confidently predicted that inflation would become a serious problem — and would have been shocked to find out that across the United States, Europe, and Japan, it has generally remained well below two percent.

So where did all the inflation go? It went into capital assets, such as treasury bonds, real estate, and stock market equity. The sort of things that benefitted directly from QE. The sort of things that rich people own.

For most people, a house is the largest asset they will ever possess; the median U.S. homeowner has more than two-thirds of their wealth tied up in a principal residence. For the richest Americans, by contrast, a principal residence accounts for just 7.6 percent of their total wealth, according to research by economist Edward Wolff. Instead, he finds that even though “almost half of all households owned stock shares [in 2016], the richest 10 percent of households controlled 84 percent of the total value of these stocks.”

Wealthy equity holders were hit hardest initially after the market crashed in 2008, then profited tremendously from the subsequent monetary stimulus. Wealth inequality in America thus shrank briefly before rebounding to record levels today (Figure 4). For all of Steve Bannon’s backward nationalist ideas, he’s right on at least one count: the owners of those assets during the last decade enjoyed “the greatest run in history.”

QE is ultimately a rehash of the beleaguered theory of “trickle-down” economics, whereby money is gifted to rich owners of capital in the hope that they will invest those new funds to create jobs for the rest of us. It’s usually done through tax cuts for the rich, but in the case of QE it’s accomplished by purchasing their distressed assets in times of trouble using money that didn’t exist before. Needless to say, the wealth doesn’t necessarily flow downward. Yet the notion dies hard because it is typically the wealthiest members of society who get to make the rules, and they’re fond of protecting themselves first.

The monetary intervention helped the western world recover from the Great Recession, but perhaps only temporarily. The Fed is currently in the process of “unwinding” QE — removing money from the economy — that it began in 2017, but it remains unclear how the market will react to being weaned from the stimulus to which it has become accustomed. The growing gap in wealth inequality is proof, moreover, that economic growth is not inclusive. Summers urges policymakers to recognize the limits of monetary policy and lean instead on fiscal policy, not as a matter of political ideology but as one of “economic reality.” There is no other way to fight secular stagnation. Summers continues:

[Secular stagnation] is the deep cause of the financial crisis. After all, during the 2003–07 period the U.S. economy did fine overall. … And yet what did it take to propel it to “fine”? It took what we now see as a vast erosion of credit standards and the mother of all bubbles in the housing market. Without those things, growth would have been inadequate in 2003–07.

…[The] structural tendency toward too much saving relative to investment is both the reason why we have sluggishness now and the reason why the periods of robust growth increasingly prove not to be sustainable.

Reflect on that for a moment. In this era of secular stagnation, rapid economic expansion is an illusion. The last two periods of bumper growth — the latter half of the 1990s and the mid aughts — were in hindsight revealed to be unsustainable credit bubbles that ended with the Dotcom crash and the financial crisis. Viewed in this context, especially given the Republicans’ unnecessary 2017 tax cut, the current period of extended economic growth is worrisome.

Rather than giving handouts to the rich, common sense would recommend redistributing wealth using progressive fiscal policy. Taxing the wealth of the ultra-rich more heavily, and using that revenue toward social programs, addresses at least part of the savings/investment imbalance by turning a chunk of those excessive savings into consumption.

The Blueprint

It’s all fine and dandy to say we should raise taxes, but none of that will matter if they’re implemented in the wrong fashion. Some types of taxes would be inimical to economic growth, and others are just too easy to avoid.

Recalling Michael Dell’s situation, for instance, a higher income tax would be an ineffective way of raising revenue from the richest citizens. Moreover, it’s a bad idea to tax income steeply because it punishes effort, which diminishes the economy’s productivity.

Economics nomenclature is a bit confusing because what most people mean by “investing” is actually saving to make a return. Increasing the capital-gains tax could thus be effective to discourage excessive saving, particularly by the wealthy. But raising revenue in this way is not straight-forward. Economist Daniel Heil warns that they could be dodged by deferring realizations until the owner dies, and passing the property on to their beneficiaries as inheritance. There are better ways.

First, plug the leaks. Close loopholes like the mortgage-interest tax deduction in the U.S., which rewards rich homeowners while inflating the housing market. Also scrap the carried-interest tax deduction, which allows hedge-fund managers — who, let’s not forget, are among the richest people out there — to pay the 20 percent capital-gains rate on the commission they earn instead of the higher income tax rate. Finally, get rid of the “stepped-up basis” loophole that exempts assets from capital-gains tax if they are passed on as inheritance.

Of course, it would be simpler to just tax inheritance, full stop. According to a 2016 study, financial inheritances dramatically worsen the inequality of life chances:

More than 50 percent of the correlation between the wealth of parents and the wealth of their children…is attributable to financial inheritances. This is more than the impact of IQ, personality, and schooling combined.

Canada, strangely, is the only country in the G7 without an estate tax. As of 2017, the U.S. taxes inheritance exceeding $11 million at a 40 percent marginal rate. Seeing that this tax now only affects the richest 0.1 percent of estates, reducing the generous exemption level would be a positive step forward. Still, those wealthy enough to pay the estate tax will fight tooth and nail to avoid it by establishing trusts, foundations, and offshore accounts. Smart policy is designed in a way that makes tax avoidance very difficult. Property tax is effective because any activity requires a physical place to operate. Even then, though, the super-rich have less than a fifth of their wealth stored in real estate on average, according to economist David Macdonald.

The best progressive tax policy is one that’s part of Elizabeth Warren’s presidential platform. Two prominent economists who specialize in studying wealth inequality, Emmanuel Saez and Gabriel Zucman, are behind her proposal for an annual wealth tax on the richest Americans. The plan would set a 2 percent recurrent tax on personal wealth over $50 million, and an extra 1 percent surtax (for a total of 3 percent) on wealth over $1 billion.

To my ears, 2 and 3 percent actually sounds too small, and the $50 million exemption, too high. In my article How Much Money Is Enough?, I argue there should be a wealth cap decidedly lower than that. But for the sake of introducing new policy ideas incrementally, and for fear that a higher tax would be harder to enforce, Warren’s proposal makes sense as well.

There are some who disapprove of the idea. Richard Epstein believes that a high-roller wealth tax would threaten economic growth, and says the rich pay an unduly large share of overall taxes as it is. He also points out that the administrative costs of a wealth tax could be prohibitive, because it can be very hard to establish a valuation of someone’s total wealth in the first place — if it hasn’t been hidden already.

Okay, deep breath.

First of all, the economic growth angle is a scare tactic torn straight from the “trickle-down” textbook, which by now serves better as bonfire kindling than useful advice. Second, the share of current taxation that the super-rich pay is irrelevant if the overall amount they pay is insufficient. A 1 percent segment of the population that owns 40 percent of the wealth is clearly not paying enough tax.

The plutes’ worst nightmare is for ordinary people to realize what’s really going on.

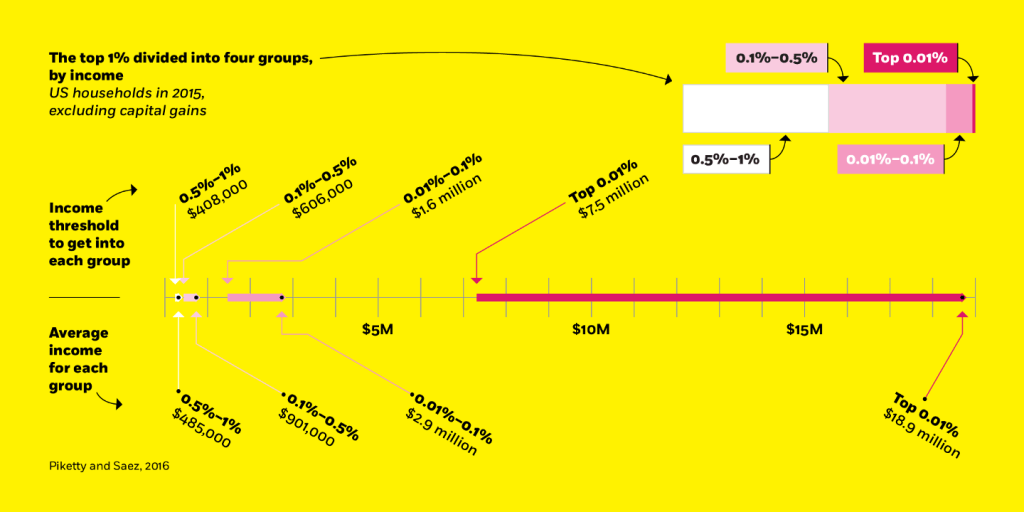

The most common and enduring criticism of progressive taxation is that instead of impeding top earners, we ought to focus on addressing the reasons for why the bottom 50 percent is struggling. But what if those elites’ overwhelming success is a reason for the difficulties of the working class? If the secular stagnation theory is correct, the super-rich bear sizable culpability for precluding a higher rate of economic growth that could be possible — in addition to capturing the lion’s share of whatever new wealth is, in fact, created (Figure 6). Far from slowing growth, a redistributive wealth tax could actually accelerate it by allocating capital more evenly.

The valuation problem, however, is a serious obstacle for a wealth tax scheme. Such a tax would provide more incentive than ever to hide money in creative ways. Furthermore, for those whose wealth barely exceeds the $50 million threshold, the government may well spend more in administrative costs than it actually raises in revenue. Yet the only alternative is to tax fewer oligarchic fortunes, preserving a status quo in which wealth steadily accumulates at the top of the pyramid. A relatively small wealth tax is worthwhile if for no reason other than to set a new, progressive precedent, akin to saying: The present, unjust state of affairs will no longer be tolerated.

We’re Done Asking Nicely

The plutes’ worst nightmare is for ordinary people to realize what’s really going on. Economic growth is exclusive, not inclusive. The majority has very little, a minority has most, and a tiny few have way too much. Within many countries, according to Zucman, the average top 0.1 percenter is 100–200 times richer than the average person. Do you think even the lowest earner, the single mom working two minimum-wage jobs, puts in less than 1/100th the effort of the CEO?

Capitalism, in it’s current form, no longer provides for everyone. Even the most devout disciples of laissez-faire fundamentalism should favour meaningful compromise to avert a mass overreaction toward authoritarianism, be it socialist or fascist. Technocratic solutions, such as universal basic income, will be expensive and complicated, but we must understand that “the only simple solutions,” as Matthew Stewart writes, “are the incredibly violent and destructive ones.”

Deep down, most people are capable of recognizing when change is overdue, even if some remain in denial until the eleventh hour. Like a desperate dictator who, with an angry mob banging on the palace gates, announces token reforms in a vain attempt to keep his throne, many of the world’s oligarchic elite engage in philanthropy. Fine, maybe that’s a bit harsh. Rich people are people, too, after all. I assume they feel compassion like anyone else. Many of them, gracious as they are, have pledged to give away much or most of their fortunes, and leave themselves with nothing but a few hundred million dollars. My point is that we ought to view these gestures less as generosity than as fractional fulfillment of profound responsibility.

Author and firebrand Anand Giridharadas is skeptical of the philanthropy paradigm because “it depends on and trusts the voluntarism of the people with the most to lose from change to be our changemakers.” A billionaire who makes a fortune in fossil fuels and then donates money to preserve coral reefs is repairing with his right hand what he’s destroying with his left. It’s not just deficient, it’s insulting.

Things are going to have to change. We’re done asking nicely.

All Rights Reserved for Brad Stollery

All Rights Reserved for