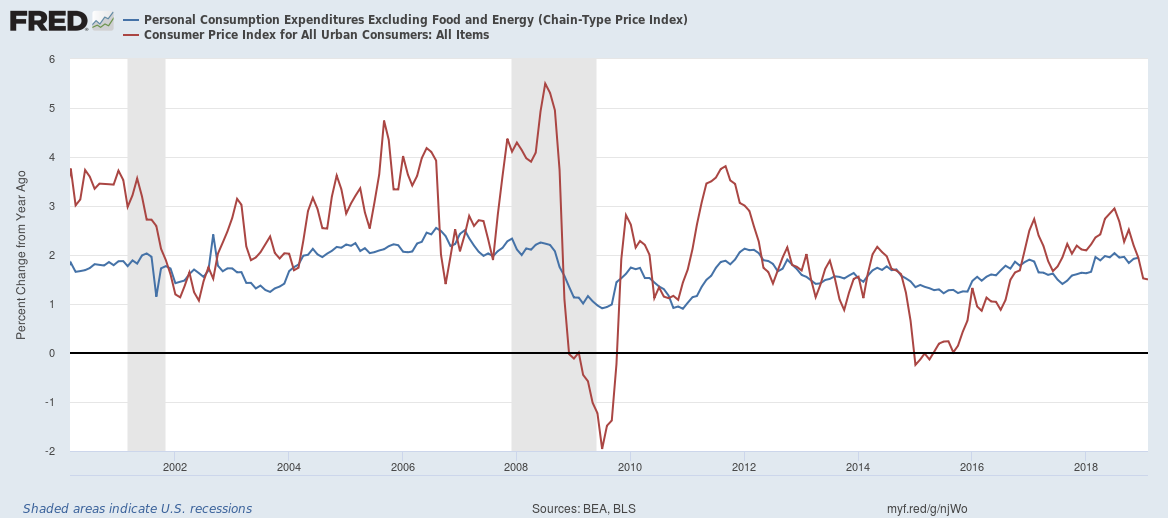

Since the onset of the 2008 recession, inflation has remained persistently low. This puzzle has some of the nation’s top economists searching for answers, with major implications for both fiscal and monetary policy tied to the various theories.

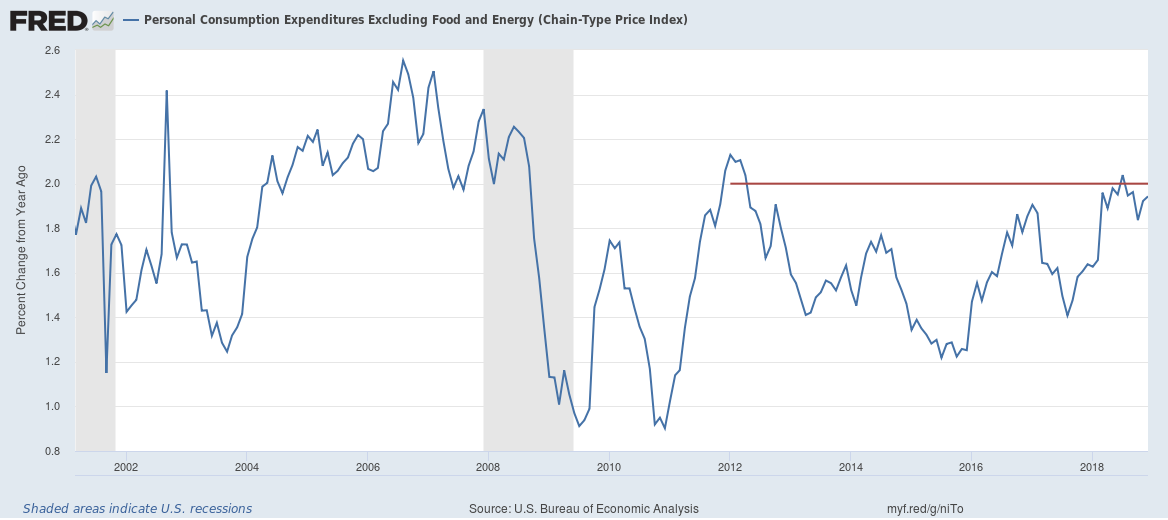

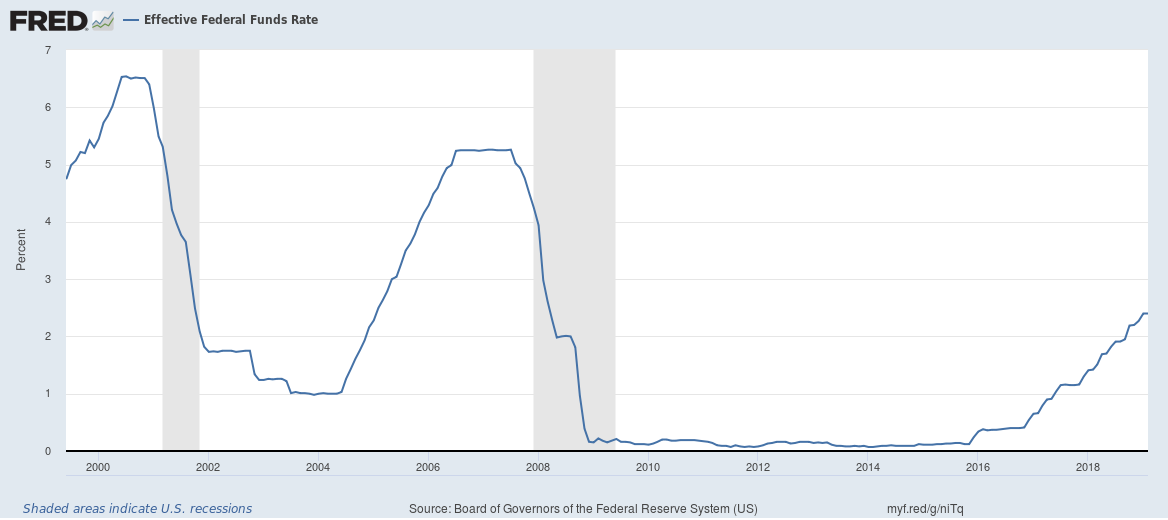

Since the 2012 introduction of an official 2% inflation target, the Fed’s preferred inflation metric (the Core PCE) has remained consistently below it. This is particularly odd, given that interest rate hikes have been steady and less aggressive than in previous recoveries. Interest rates currently sit at about 2.4%, well below their pre-recession levels.

This is particularly interesting as unemployment rates have fallen to near-historic lows. As of February 2019, the unemployment rate sat at 3.8%.

Typically, such low low unemployment rates produce rising inflation. However, the expected inflationary pressures have failed to materialize in this situation. But why?

Let’s explore the various theories and factors around this phenomena.

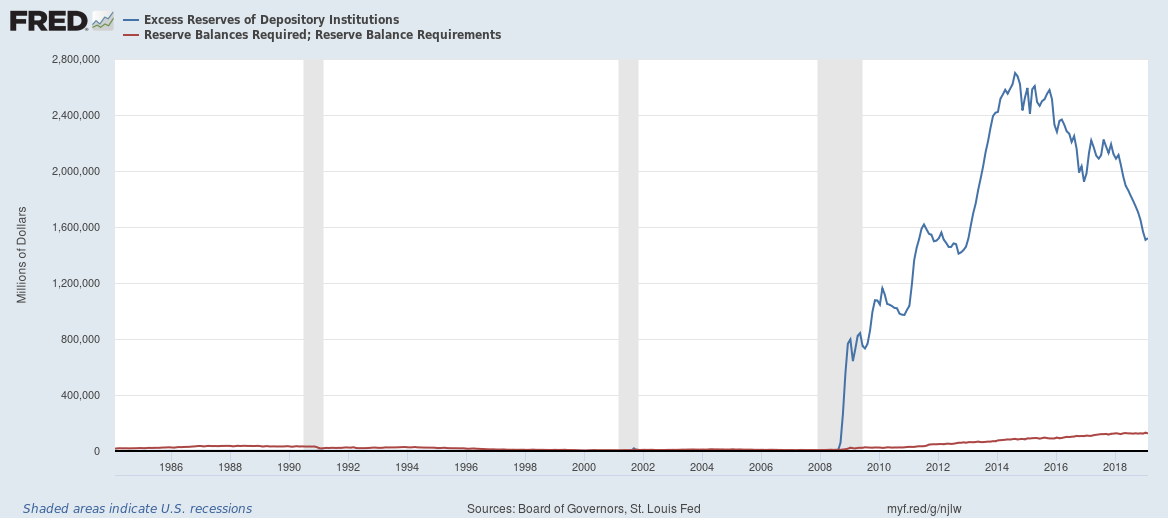

Interest On Excess Reserves

Starting in 2008, the Federal Reserve made the decision to pay interest on excess reserves. The effect has been dramatic:

Before the change, there was no incentive for banks to hold more reserves than required. However, since then reserves have ballooned to a peak of almost $2.8 trillion. Excess reserves have since tapered off to around $1.52 trillion, but this still represents a level far over historical norms. Before 2008, excess reserves were quickly spent, which pushed prices higher. Now, large quantities of money sit at the Fed collecting interest.

If this is a contributing factor, then it leaves some interesting choices. Economists such as Scott Sumner have argued that interest on reserves should be abolished — the Fed could move back towards using Open-Market Operations to control the Fed Funds Rate (FFR). It also leaves open the possibility that an influx of money from reserves could cause an unexpected inflation spike.

Labor Market Slack

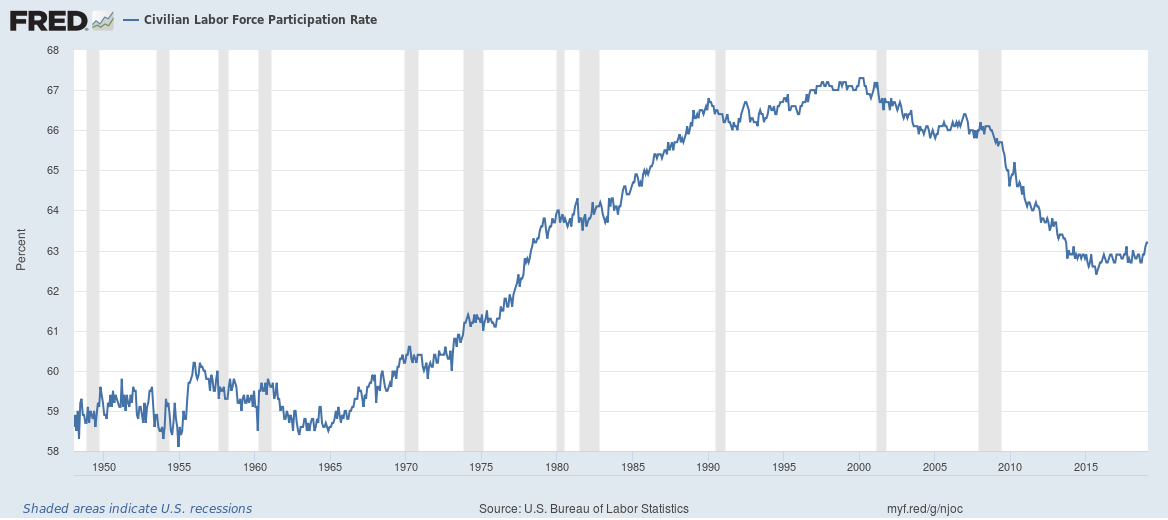

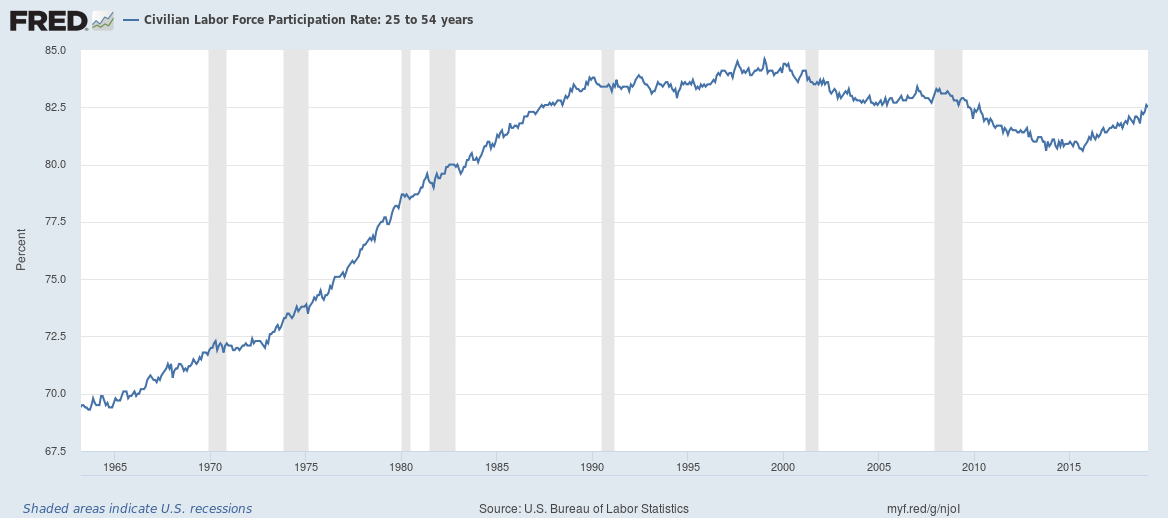

Another possible explanation is that the labor market has more slack than the Fed thinks. While unemployment is sitting at levels below 4% (and differently defined measures of unemployment are also low), some other metrics of the labor market suggest there might be some room left. One such metric is the labor force participation rate.

Much of this decline can be attributed to the aging of the population, so most economists instead choose to look at “prime age” labor force participation (which includes people ages 25–54).

The change is this chart is less dramatic than the first, but still does show participation at rates below the levels we saw from 1990 to the early 2000’s, when participation generally hovered between 83–85%. The current rate, as of February, is 82.5%. In support of this theory, the rate has been trending upwards for the past several years. Perhaps the labor force has more room to move than we anticipated?

On the other hand, much evidence indicates this might not be true. The prime-age rate has now recovered to rates very similar to the ones we saw pre-recession (when very few people would have argued the labor market was loose). Some other data also throws a wrench in this argument.

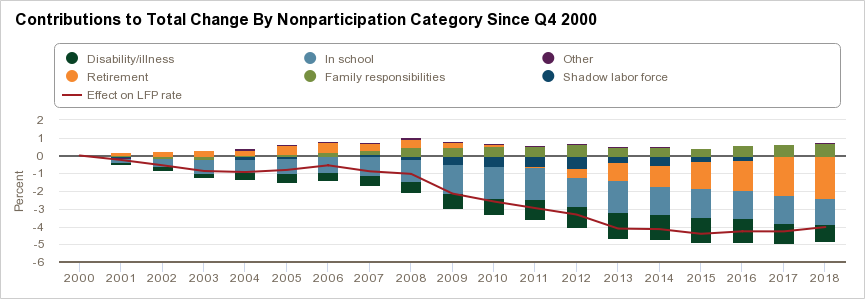

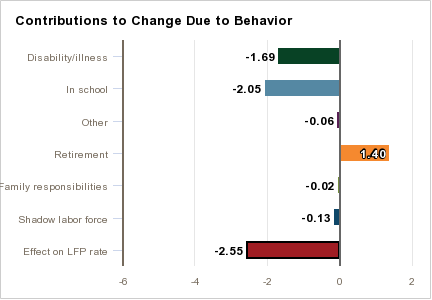

Decomposing the change in labor force participation since 2000, participation has dropped around 4%. 1.5% of this change can be attributed to shifting demographics. However, that still does leave a 2.55% gap that might constitute some excess slack.

We can see that the 2.55% reduction in labor force participation has been driven by an increase in schooling and disability/illness. Disability/illness is not a category that is typically responsive to shifting labor markets. However, schooling is known to fluctuate with labor market conditions. This share has been relatively stable in recent years though, even as the labor market improved. Most of the movement has come from the retirement and shadow labor force categories. This suggests that the declines in labor force participation can be attributed to more structural reasons.

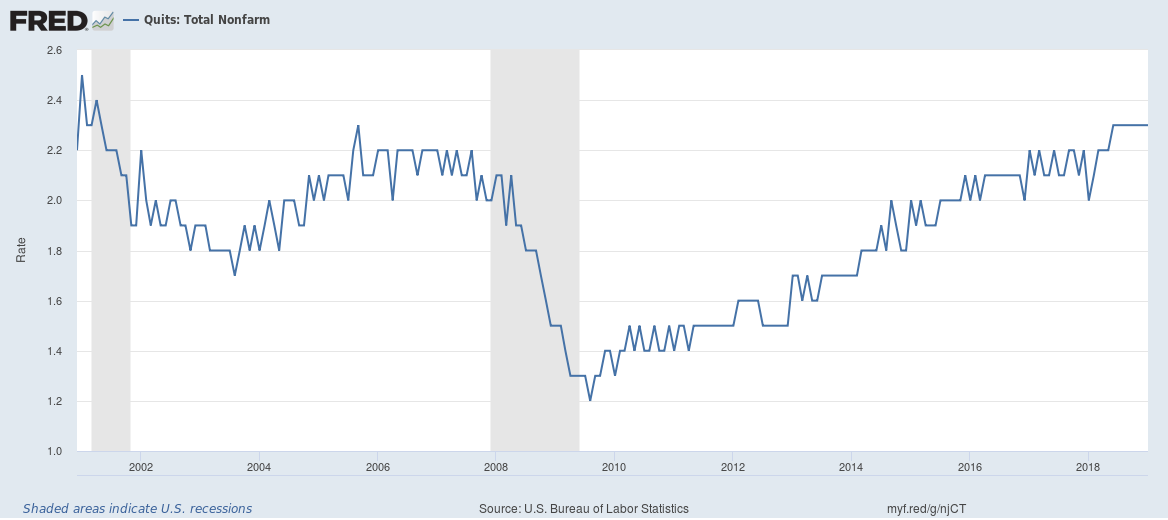

Other metrics also point to a tight labor market, including the quit rate.

The quit rate has returned to pre-recession levels, indicating workers are confident in quitting their job that they will be able to find another one.

Secular Stagnation

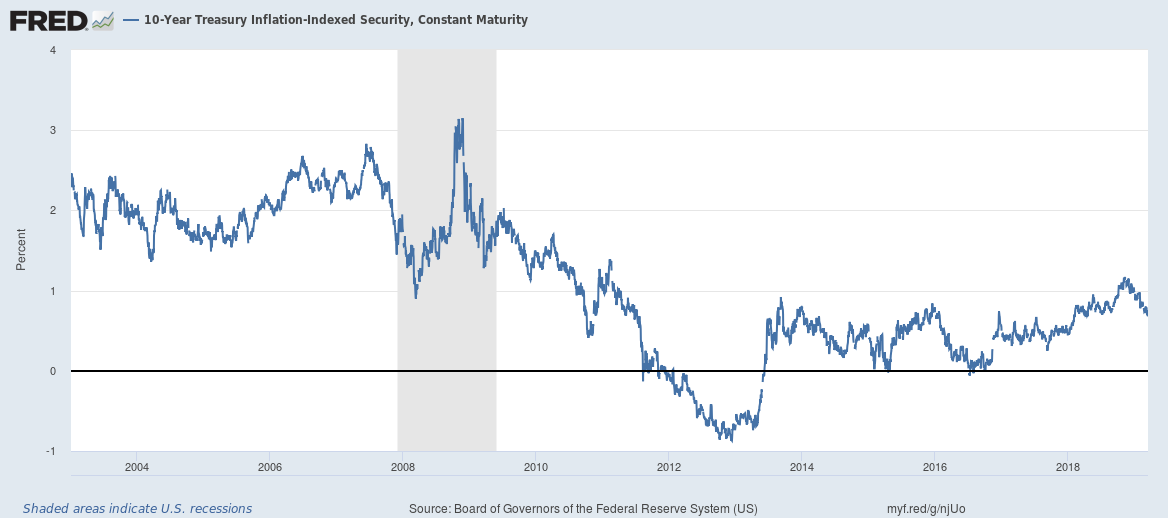

Another explanation is a ‘secular stagnation’ — a theory growing in popularity by the day. The theory was originally brought up by Harvard economist (also former Treasury Secretary and head economic adviser to President Obama) Larry Summers. The theory argues that the aging population has caused structural changes in the tendency to save against the tendency to consume, and provides explanations for persistently low real interest rates, as well as subdued inflationary pressures. Summers points to low yields on government bonds as evidence of this theory.

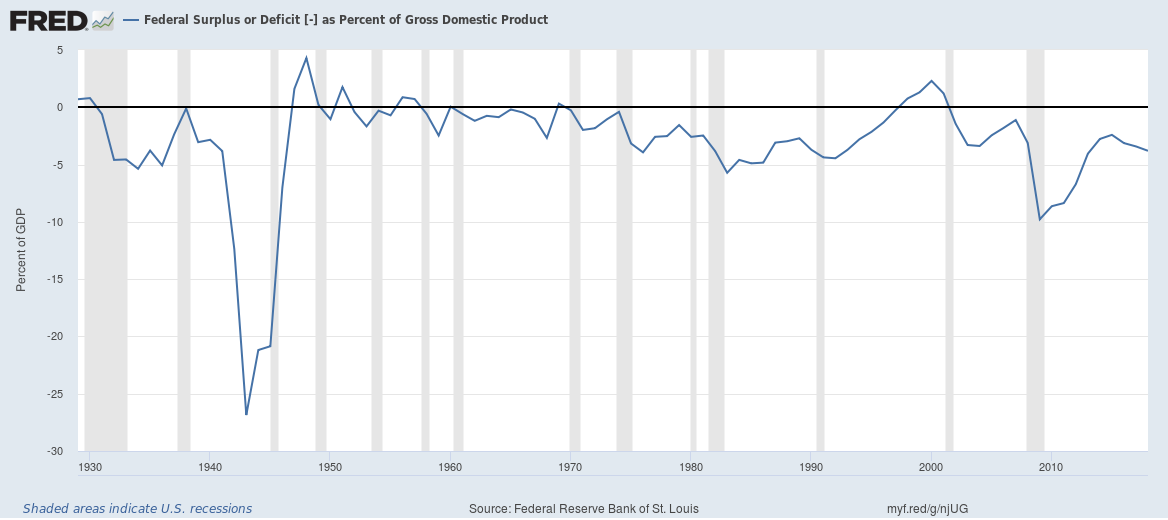

This is particularly odd in an environment of fiscal deficits, which are relatively large by historical standards.

Standard economic theory would suggest that fiscal deficits should push up real interest rates, but instead they remain anemic. Secular stagnation provides compelling explanations much of the current economic conditions.

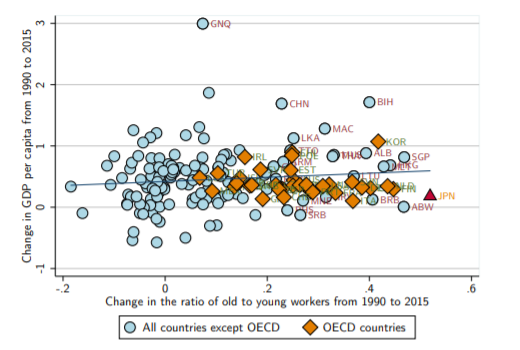

However, some other economists doubt this theory. MIT economist Daron Acemoglu released a paper that threw some cold water on the theory, showing that the link between aging and low GDP growth doesn’t hold up in cross-sectional data. In fact, countries that have experienced more aging show a positive correlation with GDP growth.

This paper also showed that these same countries also adopted more automation during that time. While the paper did not prove causal links, this presents convincing evidence that secular stagnation might not be a complete explanation.

If secular stagnation does prove to be a cause of low inflation, then Larry Summers argues that budget deficits will be needed to keep aggregate demand up and absorb private saving, while accomodative monetary policy and structural changes can be used to stimulate private investment.

Expectations

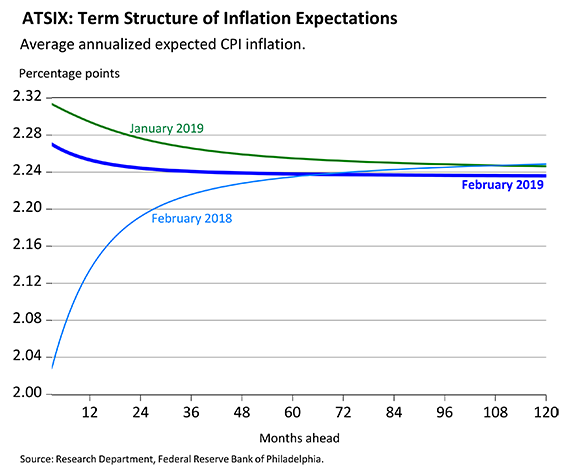

Many of the economists at the Federal Reserve are increasingly pointing to inflation expectations as the most important factor in driving inflation.

Although the evidence for this theory is still uncertain, if it is true, it would provide a very optimistic explanation for central bankers. After all, inflation has primarily undershot 2%, which could have re-aligned expectations to see the target more as a ceiling rather than a symmetric target.

It could also mean the inflation problem is now solved. In recent months, inflation has hung very close to the 2% mark, and even slightly exceeded it at one point. The Aruoba Term Structure of Inflation Expectations (from the Federal Reserve Bank of Philadelphia) show CPI expectations anchored between 2.24–2.28%.

It should be noted that the Fed targets the core PCE measure, and CPI is known to run slightly higher on average. CPI will also be more volatile, since the core measures excludes items like food and energy that are prone to large swings.

However, this suggests that the Federal Reserve should have no problem hitting their target in the coming months.

Export Shocks

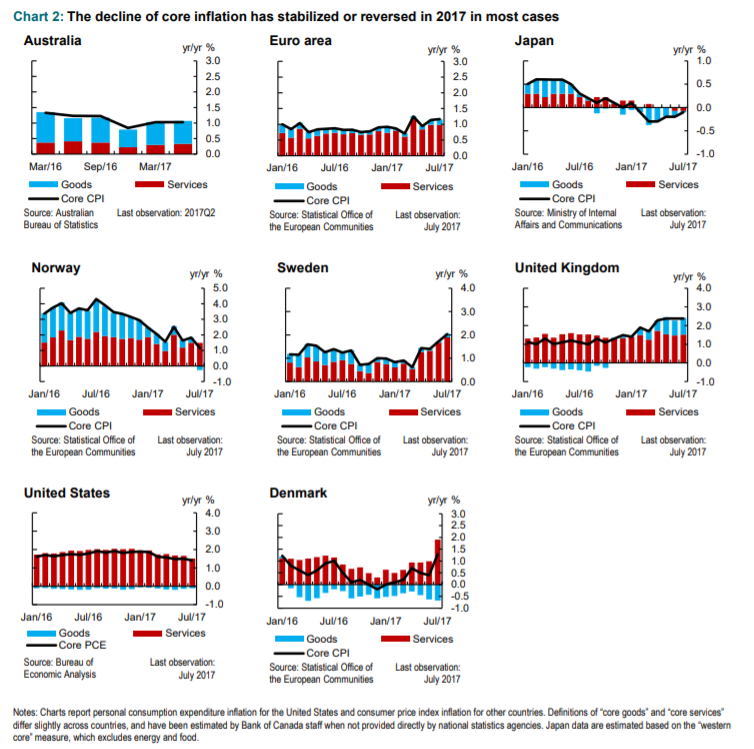

In the midst of all of this, economists at the Bank of Canada released a paper in October of 2017 that provided considerable insight.

Using data from a panel of developed countries, they noted that low core inflation metrics generally stabilized or rose through-out 2017.

While I don’t have updated charts for the past year and a half, the US experience shows that core inflation has continued to climb close to target.

The paper blames much of low inflation on cheap imports, primarily from China. The paper suggests that these factors are not likely to continue moving forward, suggesting low inflation will be less of a problem presently.

It also examined the Philips Curve, finding that although the relationship has weakened, it remains positive and significant. This mixes well with many other economists, such as President of the St. Louis Federal Reserve James Bullard, who argues the Philips Curve relationship has weakened.

This could suggest higher inflation going forward, but more room for error if monetary policy is too easy.

All Rights Reserved for Brayden Gerrard